The Consumer Data Right roll-out

Moving on from the initial roll-out phase, Open Banking today is no longer just about the big picture – it’s about the details. As the government slows the CDR’s push into other industries, the focus returns to making Open Banking as effective as possible.

In action

Banks, Trusted advisers and Fintechs all have their role to play in delivering value through Open Banking. But how use cases are unfolding in the real world (and who’s leading the charge) may be a surprise.

Showcase

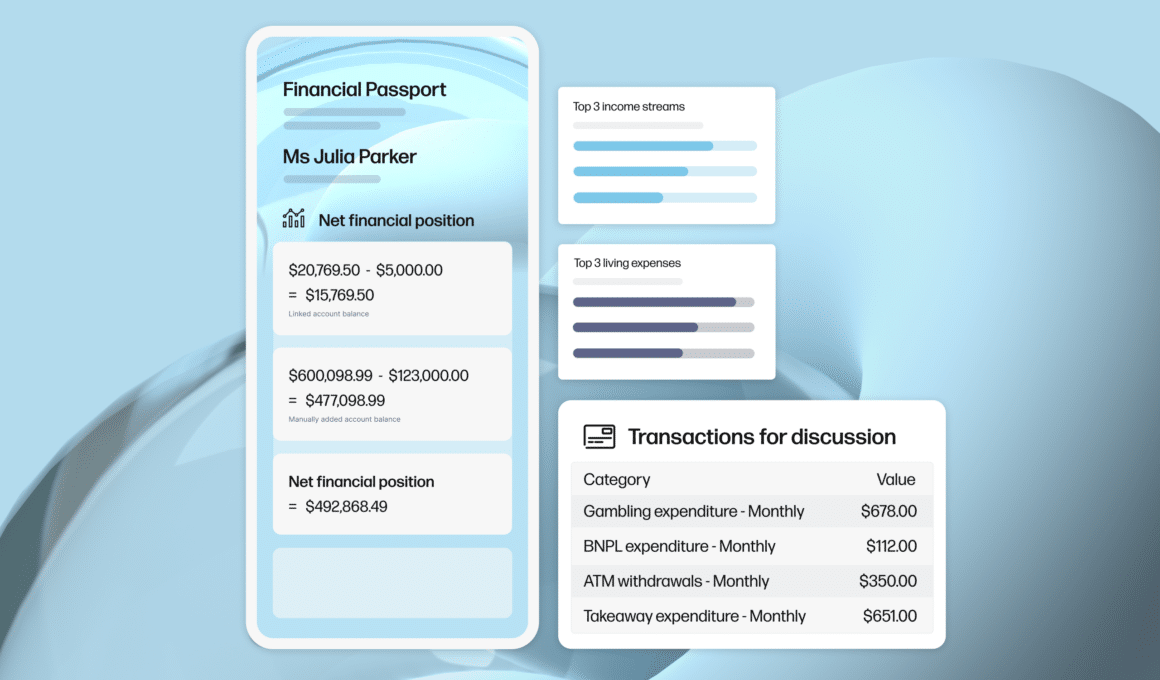

An important objective of the State of Open Banking is to inspire the industry by showcasing organisations that are using Open Banking in interesting ways. Click below to learn more about how Sherlok, AMP Advice and Waave are innovating with Open Banking.

Interviews

More from industry leaders

Over the past twelve months, we spoke with a number of other industry leaders about their views on Open Banking, and the challenges and opportunities is presents for businesses. You can find a selection of those interviews below.

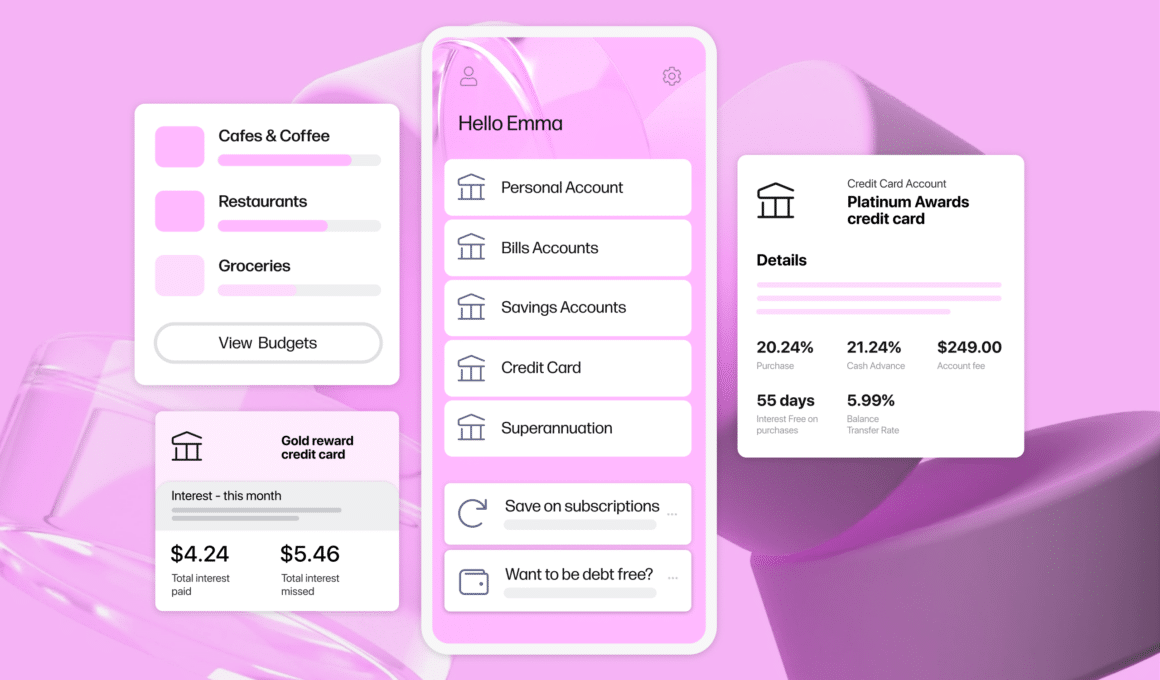

The Frollo Open Banking platform

Download The State of Open Banking 2024

Complete the form below and we’ll email you the State of Open Banking 2024 report.